The Warren Buffett Portfolio by Robert G. Hagstrom

Investing Book Notes #001

👋 CMQ Investors,

This content is free for you to enjoy. Free subscribers received these book notes in their inbox when it was originally published on September 26, 2020.

Never miss an opportunity to get a little bit wiser about investing.

How can you replicate the investing performance of Warren Buffett? More specifically, how do you construct and manage an investment portfolio that beats the market rate of return over the long-term? This is the question that The Warren Buffett Portfolio (1999) attempts to answer. Read my complete notes on Robert Hagstrom’s book below:

How did you learn about The Warren Buffett Portfolio?

I discovered The Warren Buffett Portfolio while watching a Berkshire Hathaway shareholder meeting video (see end of post). Charlie Munger, the Vice Chairman of Berkshire Hathaway, was asked about his book recommendations:

Hagstrom sent me chapters of his latest book on Warren Buffett [The Warren Buffett Portfolio], and I didn't read them because I thought his first book was a respectable book, but didn't contribute too much to human knowledge…

I want to quickly point out how savage of a statement that is. 🤣

…At any rate, he sent me the second book, a full version, and I read it, and I was flabbergasted to find it not only very well-written but a considerable contribution to the synthesis of human thought on the investment process, and I would recommend that all of you buy a copy of Hagstrom’s second Buffett book. …It doesn't pick any stocks for you, but it does illuminate how the investment process really works if you think about it rationally. —Charlie Munger

When Charlie Munger recommends a book, I try to read it. It’s a great way to get smarter.

Reading Notes & Quotes

What is focus investing? Focus investing is an alternative to the two dominant investment strategies i.e. active portfolio management and indexing.

“The essence of focus investing can be stated quite simply: Choose a few stocks that are likely to produce above-average returns over the long haul, concentrate the bulk of your investments in those stocks, and have the fortitude to hold steady during any short-term marketing gyrations.”

CMQ Fact: 64% of the Berkshire Hathaway portfolio is concentrated in just three stocks (Apple, Bank of America, Coca-Cola)

Warren Buffet says: “With each investment you make, you should have the courage and the conviction to place at least 10 percent of your net worth in that stock.” (pg. 11)

“…the heart of focus investing [is] concentrating your investments in companies that have the highest probability of above-average performance.”

How do you do it?

Choose 3 to 15 stocks based on the probability that the business will produce above-average earnings over the next decade.

“No one disagrees that an attractive company is one that enjoys high profit margins and generates cash earnings for its owners. The attraction continues if the net profits of the company earn a high return on the company’s equity.”

You want to choose companies “with the best chance for high economic returns” (pg. 7) over the long-term.

Gain a deep understanding of the underlying business. This will help you choose the right stocks for your focus portfolio and maintain your emotional equilibrium if/when there are extreme price fluctuations.

Develop the investor’s attitude i.e. the mental discipline to not become irrational when everyone else is. If you purchased the business at the right price (also easier said than done), then you can gain an advantage by buying more shares, assuming the underlying economics of the business have not changed.

Hold the company forever. Hold the company forever “so long as the company continues to generate above-average economic and management allocates the earnings of the company in a rational manner.”

Focus investing combines ideas from psychology, statistics, and biology. The strategy is a result of what Charlie Munger describes as multi-disciplinary thinking:

“Focus investing is a remarkably simple idea, and yet, like most simple ideas, it rests on a complex foundation of interlocking concepts.”

Hagstrom does a great job of detailing these concepts without getting too deep into the weeds. I found his chapters on the three academic subjects — as they relate to focus investing — to be extremely usable.

Probability Theory (Mathematics)

As focus investors, Buffett and Munger make big bets on what they believe are high probability events. The “event” is if a business is going to generate an above-average return over a long-period of time. If the price is right, then Buffett and Munger bet big. A recent example of Buffett and Munger exercising the focus investing strategy is the purchase of Apple Stock.

“It is a vast oversimplification, but not an overstatement, to say that the stock market is an uncertain universe. In this universe are hundreds, even thousands of single forces that combine to set prices, all of which are constantly in motion, any one of which can have a drastic impact, and none of which is predictable to an absolute certainty. The task for investors, then, is to narrow the field, to identify and remove that which is the most unknown, and to focus on the least unknown. And that is an exercise in probability.” (pg. 113-114)

For focus investors, uncertainty is a good thing: “Face up to two unpleasant facts: the future is never clear and you pay a very high price in the stock market for a cherry consensus. Uncertainty is the friend of the buyer of long-term values.” (pg. 185)

“…virtually all decisions that investors make are exercises in probability. For them to succeed, it is critical that their probability statement combines the historical record with the most recent data available. And that is Bayesian analysis in action.” (pg. 119)

“Thinking in probabilities, subjective or not, enables you to think clearly and rationally about a purchase.” (pg. 124)

“…as the probability rises, so should the amount of the investment.” (pg. 136)

Warren Buffet says: “Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily understandable business whose earnings are virtually certain to be materially higher five, 10, and 20 years from now. Over time, you will find only a few companies that meet these standards — so when you see one that qualifies, you should buy a meaningful amount of stock.” (pg. 190)

Kelly Optimization Model: “…often called the optimal growth strategy, is based on the concept that if you know the probability of success, you bet the fraction of our bankroll that maximizes the growth rate.” (pg. 126)

Behavioral Finance (Psychology)

If you follow Buffett’s guidance for focus investing i.e. by putting 10% of your net-worth in a single stock, you are going to need to maintain your emotional equilibrium. This is easier said than done. After all, holding a big position when the market tanks requires you to maintain rationality about losing money which, by nature, causes us to behave irrationally.

Mastering our emotions is more important for investors than having superior skills in mathematics, finance, and accounting. Benjamin Graham calls it having the investor’s attitude.

“…it is not an exaggeration to say that the entire market is pushed and pulled by psychological factors.” (pg. 142)

Warren Buffett says: “If you have [the investor’s attitude], you start out ahead of 99 percent of all the people who are operating in the stock market—it’s an enormous advantage.” (pg. 143)

“…people tend to overreact to bad news and react slowly to good news. Psychologists call this overreaction bias. Thus, if the short-term earnings report is not good, the typical investor’s response is an abrupt, ill-considered overreaction, with its inevitable effect on stock prices.” (pg. 143)

“In a turbulent sea of irrational behavior, the few who act rationally may well be the only survivors.” (pg. 143)

“Do not be stampeded by other people’s misjudgment. This is the lesson that Graham preached.” (pg. 144)

Remember: Focus investors do not attempt to forecast on how the psychology of the market will impact prices.

“Investment is an activity of forecasting the yield on assets over the life of the asset. Speculation is the activity of forecasting the psychology of the market.” —Keynes

Complex Adaptive Systems (Science)

We live (and invest) in a complex world. The economy itself is a complex adaptive system. Understanding the nature of complex adaptive systems is useful for focus investors. This chapter reminds me of what to avoid wasting mental energy on e.g. trying to make predictions about a stock (or the economy) based on the past, looking for patterns, etc.

The limitations of pattern recognition in a complex adaptive system:

“There are limits to pattern recognition in a complex adaptive system like the stock market.” (PG)

“If you have a truly complex system then the exact patterns are not repeatable.” — Brian Arthur (pg. 183)

Like a kaleidoscope, patterns in this world change with some apparent order but never repeat in the fact sequence. The patterns are always new and different.” (pg. 183)

The inability to predict the future with any sort of certainty makes it harder to stay rational.

“The more abstract the environment —and stocks are an abstraction to many people—the more forceful the intangible psychological factors become.” (pg. 142)

This is an example of how Hagstrom does a great job tying these ideas together.

“It is a vast oversimplification, but not an overstatement, to say that the stock market is an uncertain universe. In this universe are hundreds, even thousands of single forces that combine to set prices, all of which are constantly in motion, any one of which can have a drastic impact, and none of which is predictable to an absolute certainty.” (pg. 114)

“My gut feeling is that complex adaptive systems is a very powerful way of understanding how capital markets operate. As complex adaptive systems become better understood, I believe investors will have much better descriptions of how markets actually work.” —Mauboussin (pg. 178)

Critical Thinking

#1 — It is important to challenge conventional wisdom.

Shortly after I began reading the book, I noted how Warren Buffet is a contrarian thinker. In the early half of The Warren Buffett Portfolio, Hagstrom does an excellent job telling the history of investment theory, and in doing so, allows the reader to see that Warren Buffett went against-the-grain with his approach to investing. I think this is extremely important to acknowledge and understand, especially for new investors. Warren Buffett is now seen as the GOAT of investing and people attempt to imitate his investment strategy. But Buffett’s strategy is the product of thinking that what the ‘experts’ believed to be true, was false.

For example: When running his investment partnership, Warren Buffett disregarded the conventional wisdom about investment risk. The academics, at the time, defined the risk of an investment in terms of price volatility.

Buffett defined risk as harm or injury, i.e. permanently losing capital. This is important to how Buffett constructed his portfolio; he didn’t care about metrics like Beta. He was free from the confines of conventional thinking.

“The real risk, Buffett says, is whether the after-tax returns from an investment ‘will give him [an investor] at least as much purchasing power he had to begin with, plus a modest rate of interest on that initial stake.’” (pg. 30)

Those following financial theory — specifically modern portfolio theory — would never concentrate their investments into a few stocks because the year-to-year volatility would be extreme.

The way that Buffett thought about risk allowed him to make purchases that most professional investors would likely have advised against.

Key Quote: “If you asked me to assess the risk of buying Coca-Cola this morning and selling it tomorrow morning,” Buffett says, “I’d say that that’s a very risky transaction.” But, in Buffett’s way of thinking, buying Coca-Cola this morning and holding it for ten years, carries zero risk.” (pg. 30-31)

This also caused him, in part, to avoid the limitations of diversification. Buffett instinctively knew that diversification meant average. He wanted to beat the market.

“Indexing, because it does not trigger equivalent expenses, is better than actively managed portfolios in many respects. But even the best index fund, operating at its peak, will only net exactly the returns of the overall market. Index investors can do no worse than the market — and no better.” (pg. 5)

“According to modern portfolio theory, the primary benefit of a broadly diversified portfolio is to mitigate the price volatility of the individual stocks. But if you are unconcerned with price volatility, as Buffett is, then you will also see portfolio diversification in a different light.”

Furthermore, Buffett looked at risk more pragmatically. If you bought a business for a reasonable price, then a dip in price is a buying opportunity. There is no need to mitigate volatility if you believe in the business’s ability to produce cash in the long-term.

#2 — The importance of understanding what you are buying.

It is intellectually dishonest to claim that one factor has made Buffett the greatest investor of all time. And Hagstrom does not attempt to do this. One of these factors, though, is Buffett’s skills at analyzing the underlying economics of a business. The Warren Buffett Portfolio encouraged me to continue sharpening this skill.

Buffett believes the accuracy of your analysis of a business is a competitive advantage.

“Generally, [the great financial thinkers] all agree that speculators are obsessed with guessing future prices while investors focus on the underlying asset, knowing that future prices are tied closely to the economic performance of the asset.” (pg. 202)

“We can say with certainty that knowledge works to increase our investment return and reduces our overall risk.” (pg. 202)

If you watch any of Warren Buffett’s interviews or speeches on YouTube, he almost always makes the following points:

When you buy a company’s stock, you are buying a little piece of that business. Therefore, the thinking-process you should use when buying a company’s stock is the same as if you are buying the whole business.

You buy one business instead of another (or any asset, for that matter) based on how much cash you believe it is going to give you, and of course, if it is available at a fair price.

Key Point: If you understand the intrinsic value of what you purchase, and you plan to hold the asset for the long-term, then price volatility does not bother you. (If you are to use the focus investment strategy, the price volatility cannot bother you.) The reason is that a company’s stock price will eventually reflect the operating earnings of the business. If you have a long holding period, then the price volatility is of little-to-no-concern, so long as the underlying economics of the business have not changed.

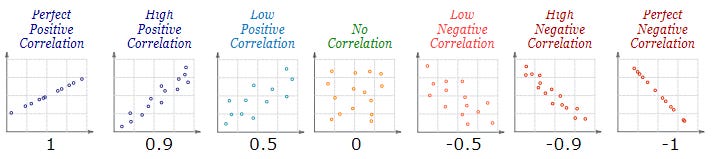

Hagstrom used a laboratory group of 1,200 companies to determine how closely price and earnings are connected. In doing so, Hagstrom discovered that the longer an investor holds a stock, the more significant the relationship is between price and earnings.

Price vs. Earning Correlation

Three-Year Holding Period: .131 to .360

Five-Year Holding Period: .374 to .599

Ten-Year Holding Period: .595 to .695

Eighteen-Year Holding Period: .688

Your knowledge of the business is a competitive advantage, and it combats the errors caused by psychological misjudgements. When there is price volatility (and there always will be), the natural reaction is to sell while you are still ahead. This is counterproductive to long-term success. One of the best ways to combat this psychological misjudgment is to know the business inside-and-out. If you are confident in the long-term economics of the business, then a rapid fluctuation in price will not cause you to act irrationally.

#3 — Long-term thinking is a long-term advantage-creator.

I see this pattern time-and-time again when reading about successful entrepreneurs. Jeff Bezos is one of the biggest proponents of long-term thinking. In his first letter to Amazon shareholders — circa 1997 — Bezos begins by saying:

It’s All About the Long Term

We believe that a fundamental measure of our success will be the shareholder value we create over the long term. This value will be a direct result of our ability to extend and solidify our current market leadership position. The stronger our market leadership, the more powerful our economic model. Market leadership can translate directly to higher revenue, higher profitability, greater capital velocity, and correspondingly stronger returns on invested capital.

Our decisions have consistently reflected this focus. We first measure ourselves in terms of the metrics most indicative of our market leadership: customer and revenue growth, the degree to which our customers continue to purchase from us on a repeat basis, and the strength of our brand. We have invested and will continue to invest aggressively to expand and leverage our customer base, brand, and infrastructure as we move to establish an enduring franchise.

Focus investing requires a long-term time horizon. Long-term time horizons help improve the probability that you will beat the market.

“For [Buffett], the moral of the story is clear: We have to drop our insistence on price as the only measuring stick, and we have to break ourselves of the counterproductive habit of making short-term judgements.” (pg. 73)

Unfortunately, most investors and fund managers suffer from investment myopia i.e. an overemphasis on the short term.

“There is substantial pressure on portfolio managers to generate eye-catching short-term performance numbers.” + “fixation on short-term price performance.”

“The unrealized capital gain in your portfolio is yours to keep as long as you own the stock. By holding on to the gain, assuming the investment tenets behind owning the company have not changed, you are able to compound your net worth more forcefully.” (192)

“Don’t overlook the value of unrealized capital gains. With the exception of passive index funds, focus investing gives you the best opportunity to compound this unrealized gain into major profits.”

Final thoughts:

This was an enjoyable read… unlike some of the other investing books I am reading for this content series.

Core thesis of the book: “The fact still remains: A focus portfolio stands the best chance of beating a market rate of return.”

However, the focus investment strategy is probably the hardest to apply.

“Investing is easier than you think, but harder than it looks.”

— Warren Buffett

It is harder to achieve breakout performance than it once was: “As more and more people become more and more skilled at investing, the odds of a breakout performance by a few superstars diminish.” (188)

Your goal as an investor: "Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily understandable business whose earnings are virtually certain to be materially higher five, 10, and 20 years from now. Over time, you will find only a few companies that meet these standards — so when you see one that qualifies, you should buy a meaningful amount of stock.” — Warren Buffett

Applying the multi-disciplinary approach to the aforementioned Buffett quote:

Probability Theory: By having clearly defined standards for what makes an attractive investment (“…an easily understandable business whose earnings are virtually certain to be materially higher five, 10, and 20 years from now…”), you can narrow down your options, and improve the probability of success.

Behavioral Finance: If you know the business inside-and-out, you will not be inclined to make an irrational decision when the price dips and/or the market tanks.

Complex Adaptive Systems: When you recognize the true nature of the system, your rational thinking is strengthened as you focus on what you can know (like the quality and value of the asset you are buying).

Finally, here is the video where Munger recommends Hagstrom’s book.

Great summary of the book, thank you! Adding this to my reading list for sure.

Love this article! A really great summary of Hagstrom’s book!